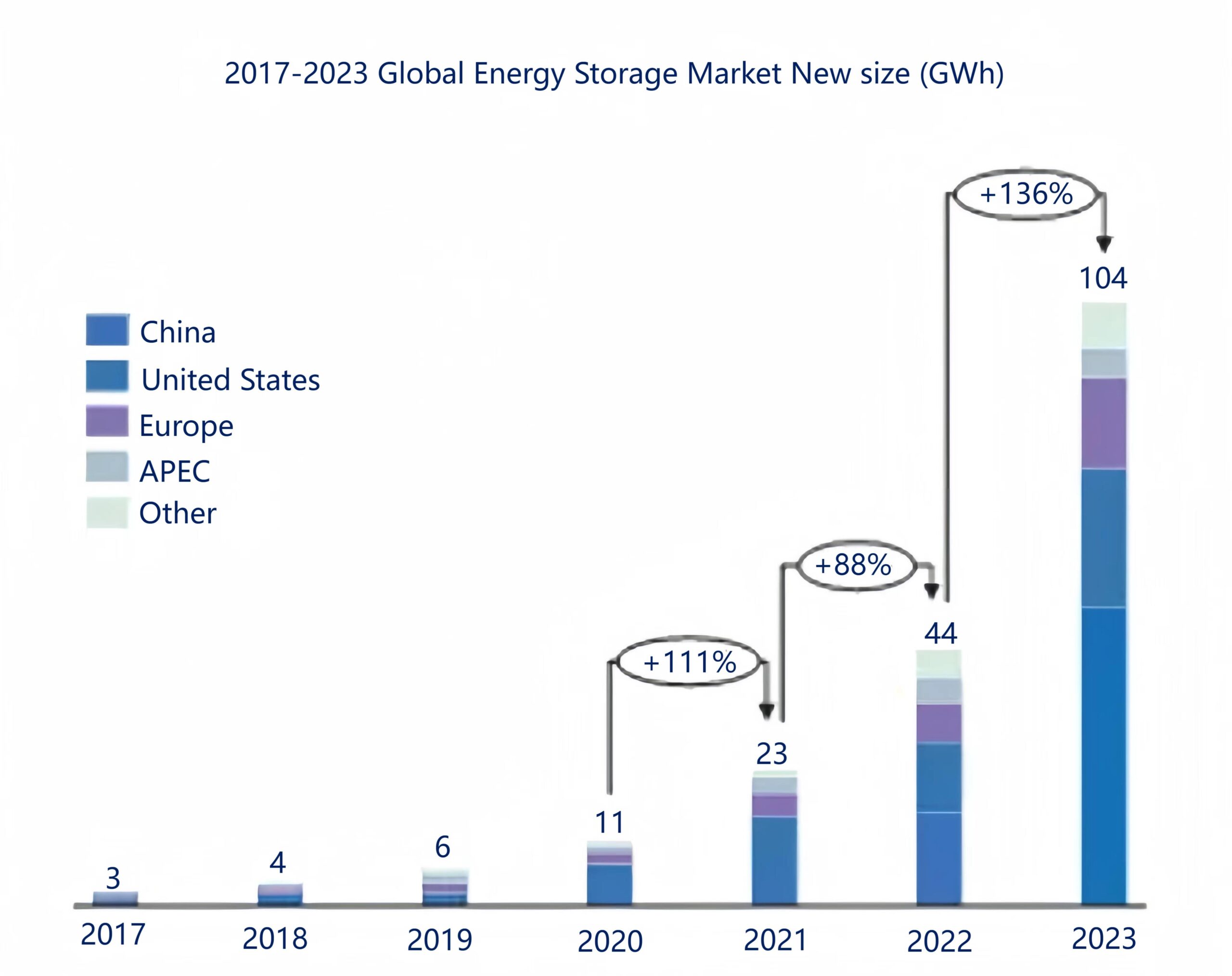

In the context of global carbon neutrality, energy transformation has shown an irreversible trend around the world. On this basis, the global energy storage market has also entered a stage of rapid development. According to EESA statistics, the average growth rate of global new energy storage installed capacity (GWh) from 2017 to 2023 exceeded 85%, especially after 2020, showing a growth trend of nearly doubling every year. In 2023, the new installed capacity of the global energy storage market will reach 103.5GWh, which has exceeded the historical cumulative scale of global energy storage installed capacity (101GWh).

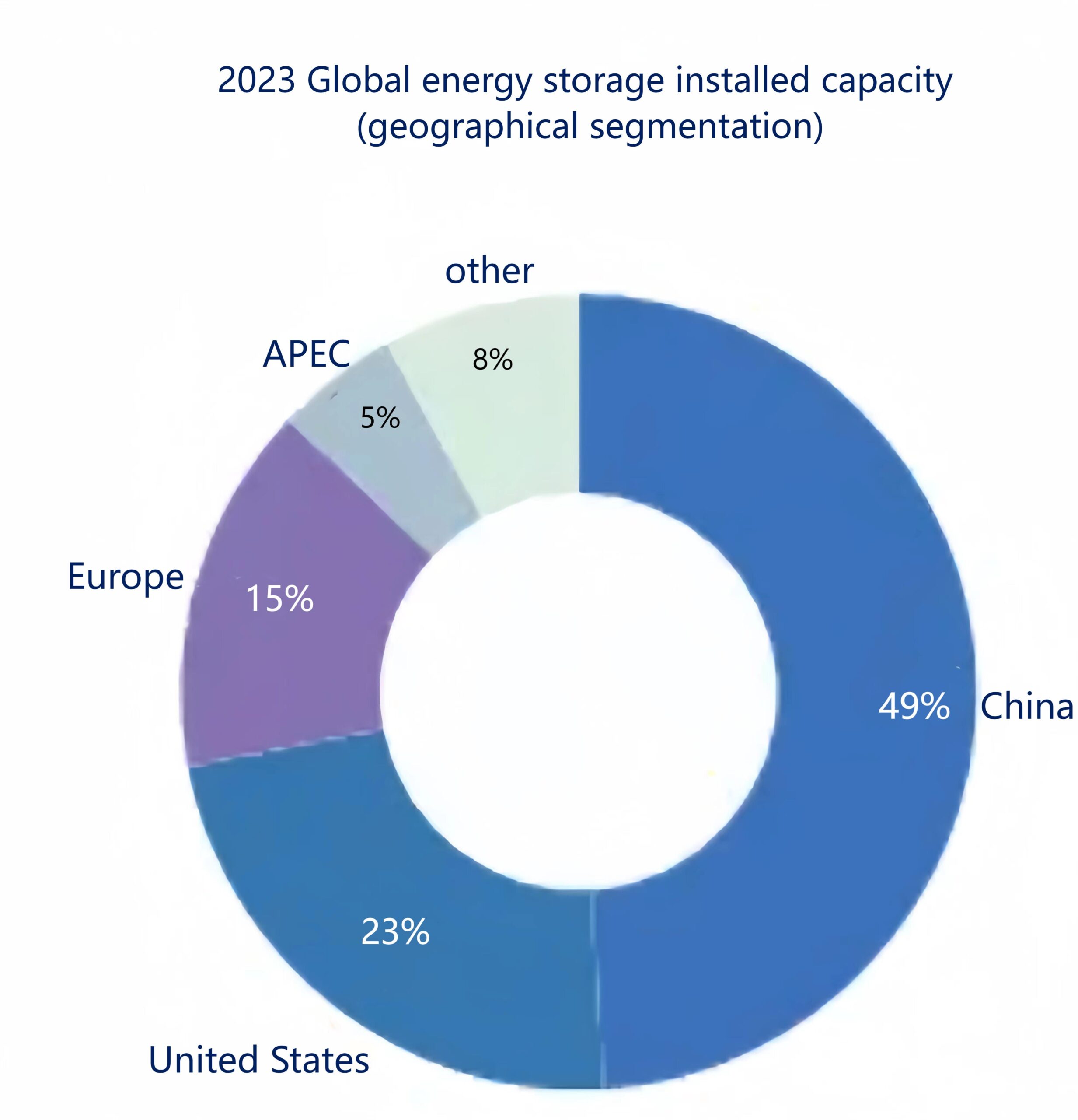

The Chinese market has always played an indispensable role in the global energy storage market. China’s energy storage installed capacity has surpassed that of the United States for two consecutive years, becoming the country with the highest proportion of new additions to the global energy storage market. According to EESA statistics, the newly installed capacity of China’s energy storage market will reach 51GWh in 2023, surpassing the United States for two consecutive years, becoming the country with the highest new share of the global energy storage market, about 49%, far exceeding the United States, Europe, Asia-Pacific, etc. other major areas.

At the same time, the global energy storage market has also shown a highly concentrated trend in recent years. The proportion of new additions in the CR3 region (China, the United States, and Europe) in the global energy storage market has remained above 80% since 2020, especially in 2023. year, reaching its highest share in history (88%)。

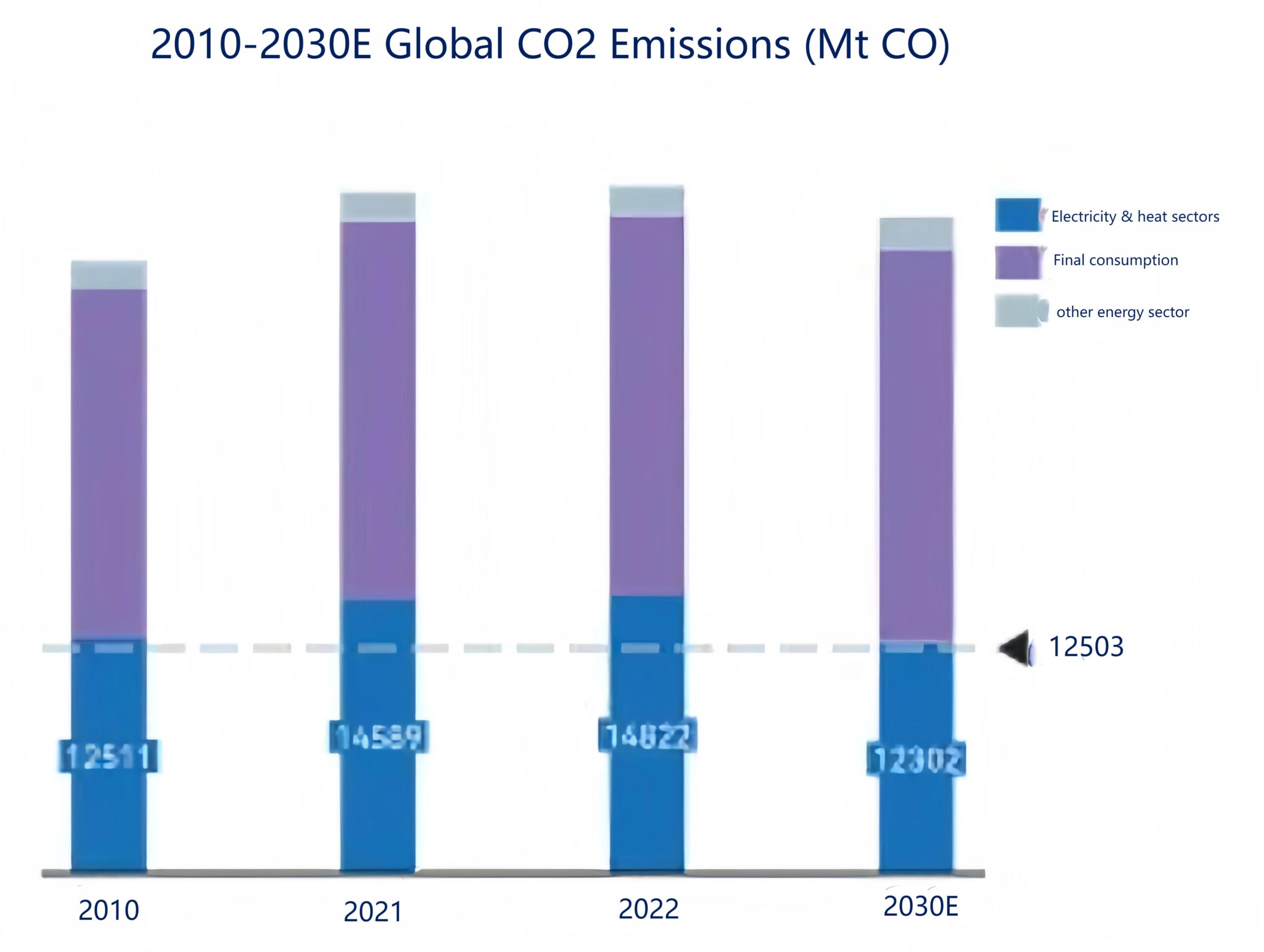

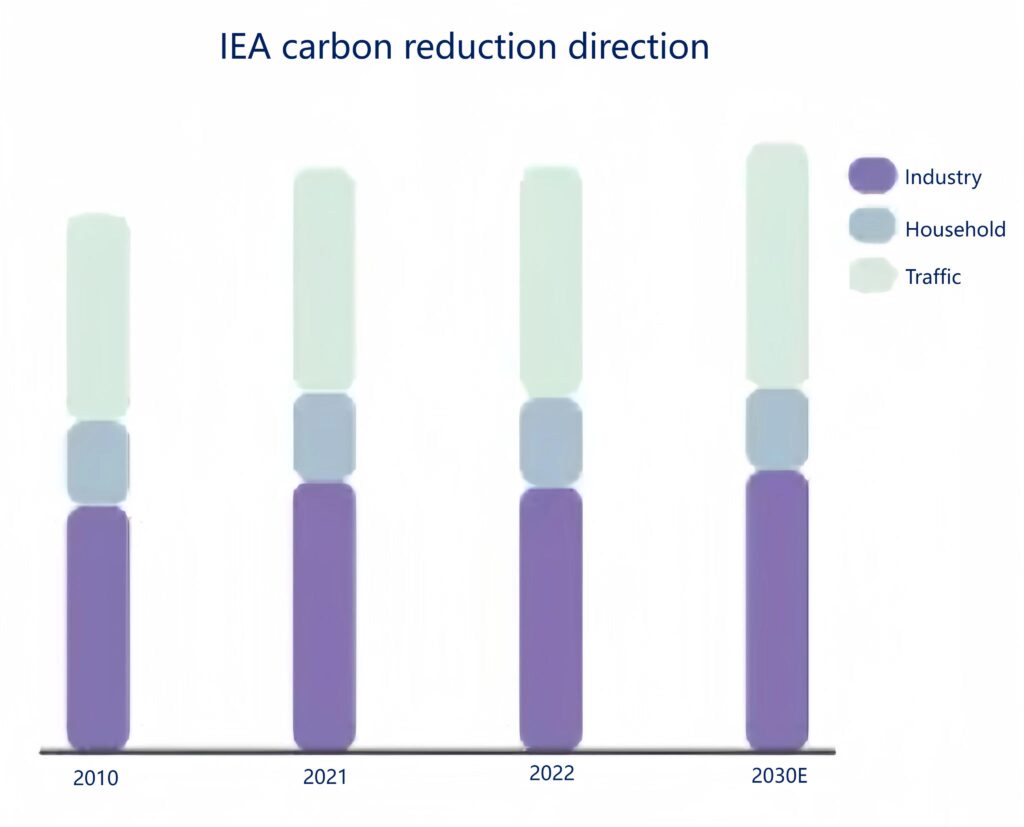

According to the International Energy Agency (IEA) “Global Energy Sector 2050 Net Zero Emissions 3 Roadmap”, global energy sector carbon emissions can be mainly divided into electricity and heat sectors, final consumption and other energy sources. Department (Other energy sector).

According to the 2050 net-zero emission roadmap for the global energy sector, in order to achieve the common goal of global carbon neutrality in the Paris Agreement, carbon emission reduction in the power & heating sector is the main direction of efforts for each country in the future, and it needs to be Reduced to levels close to 2010 (nearly 12,000 MtcO2), this is also a key factor that directly promotes the development of global source-grid side energy storage.

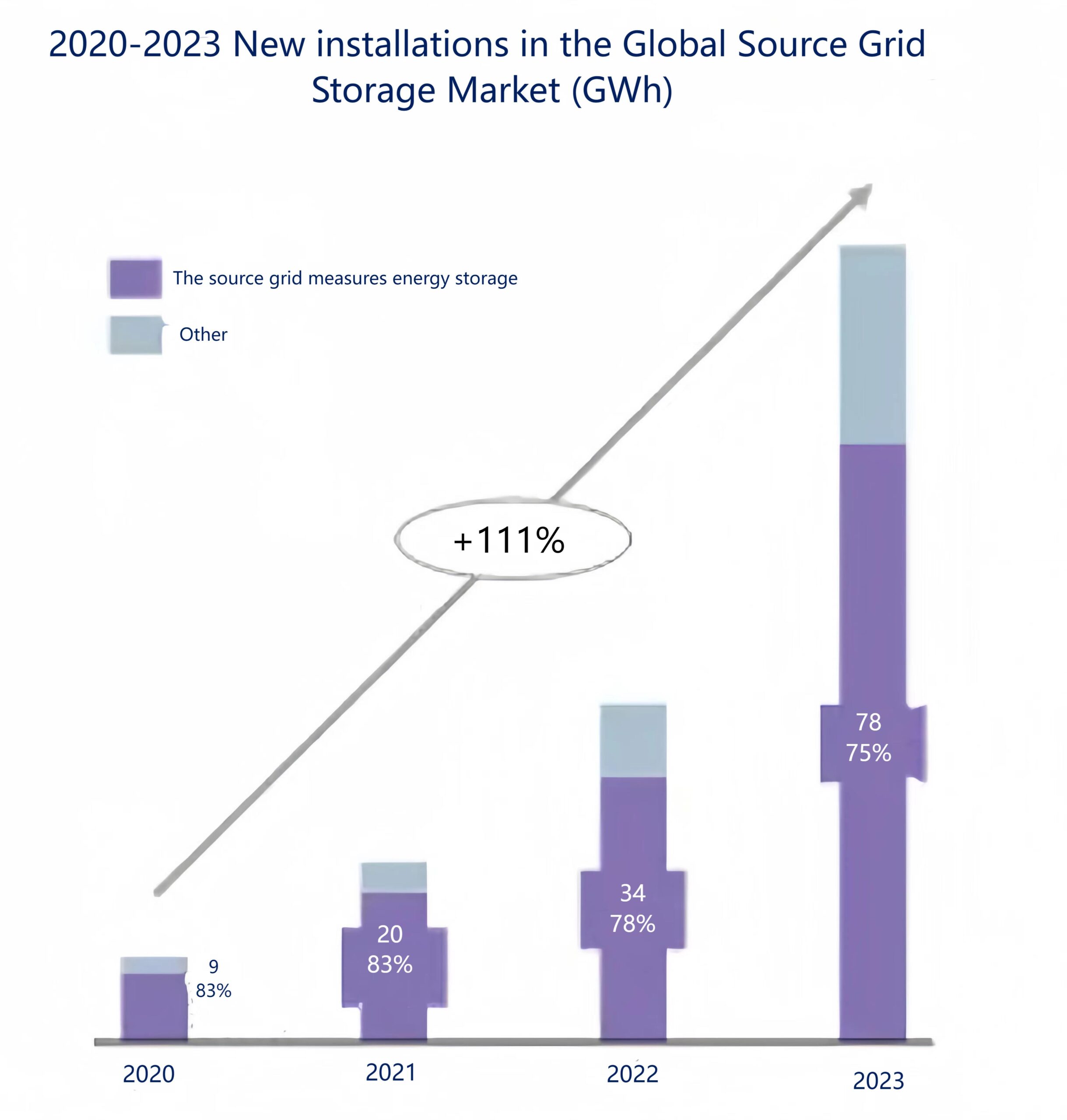

Energy storage on the source and grid side plays a major supporting role in the future global energy transformation and is also an important pillar for various countries to build new (mainly new energy) power systems. In the past development process of global energy storage, source-grid energy storage has always been the main growth point of the global energy storage market. The average annual growth rate from 2020 to 2023 reached 111%, which is equivalent to the growth rate of the global energy storage market. The growth rate is doubling every year. Although the installed capacity of the global source-grid side energy storage market is growing rapidly, the proportion of the overall new capacity is decreasing year by year. Although the data shows that the decline has not been significant in the past four years, it also reflects the global trend in recent years. The rise of the energy storage market.

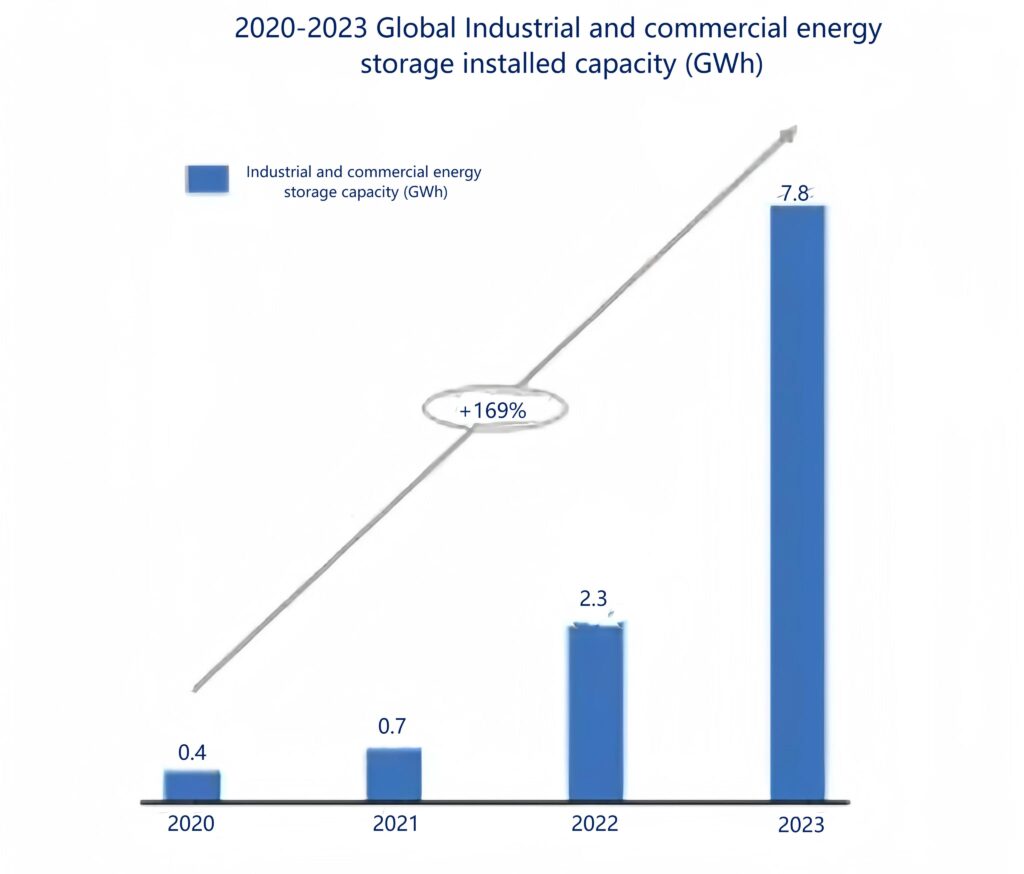

According to the IEA’s “2050 Net-Zero Emissions Roadmap for the Global Energy Sector”, the IEA divides carbon emission reduction in the end-use energy consumption sector into three major areas: industry, residential and transportation. Among them, energy conservation and emission reduction in the industrial sector is the most important on the road to carbon neutrality. one of the directions. For industrial application scenarios, industrial and commercial energy storage has been in a stage of high growth in recent years, with the average annual growth rate of global industrial and commercial energy storage reaching 169% from 2021 to 2023. The main commercial scenarios for industrial and commercial energy storage include energy conservation and emission reduction, high energy consumption transformation, integration of light storage and charging, etc.

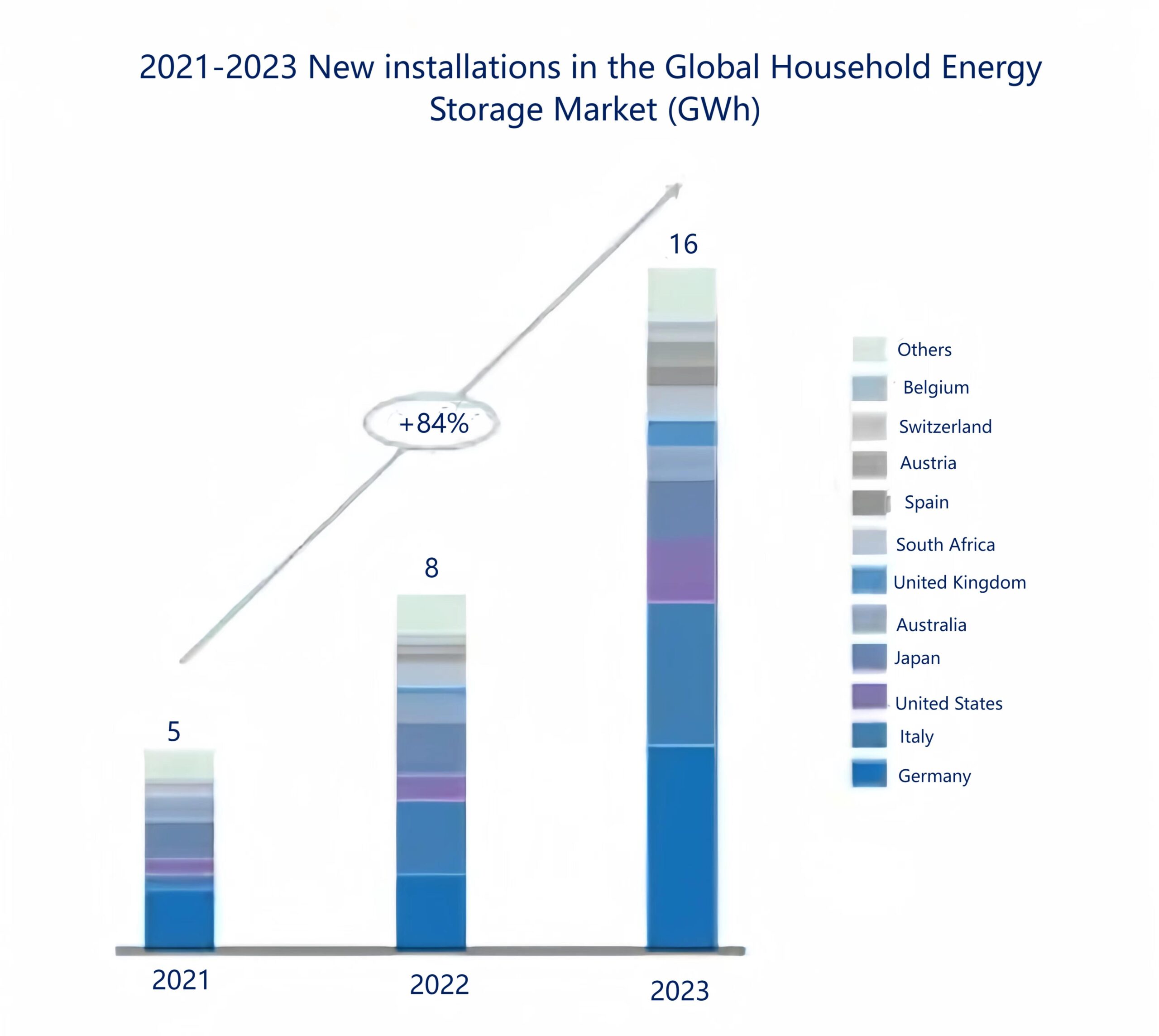

Almacenamiento de energía doméstico corresponds to the application scenario of residential energy consumption and carbon emission reduction in the IEA net-zero emission route. According to installed capacity statistics, the average growth rate of new installed capacity in the global household energy storage market from 2021 to 2023 reached 84%. According to EESA statistics, the installed capacity of the global household energy storage market in 2023 will be approximately 16.1GWh, a year-on-year increase of 91%. Germany, Italy, the United States, Japan, and Australia are still the countries with relatively good development of household energy storage markets worldwide. The total newly installed capacity in the CR5 region accounts for 71% of the global total. The markets in Germany, the United States, Japan and Australia are still household energy storage markets with relatively stable global demand.

For more information, please stay tuned for website updates, or follow our social media accounts. If you have any questions, please feel free to contact us!